CONGRESS STILL CONCEALS THE SECRETS OF THE FEDERAL RESERVE

See England Official Secrets PDF

See Colonel Edward Mandell House PDF

Chairman of the Federal Reserve - the most powerful job in the free world.

Rudy Havenstein Lashes Out: "No, The Fed Is Not Populist"

Proof that the United States of America Inc. is NOT a Corporation.

Copyright FreeAmerica and Harry V. Martin, 1995

Article I, Section 8, Clause 5, of the United States Constitution provides that Congress shall have the power to coin money and regulate the value thereof and of any foreign coins. But that is not the case. The United States government has no power to issue money, control the flow of money, or to even distribute it - that belongs to a private corporation registered in the State of Delaware - the Federal Reserve Bank.

The Federal Reserve System was established by President Woodrow Wilson in 1913. The premise used by President Wilson and his financial advisors for the establishment of the Federal Reserve System was to "supplant the dictatorship of the private banking institutions" and "to stabilize the inflexibility of national bank note supplies". The previous system of banking was "feudal" in nature, in which private bankers control communities and could issue their own bank notes. They had little regulations concerning reserve assets and loan policies. Banking was a patch-quilt of institutions scattered across the face of the nation with no central policy.

READ [Public—No. 43—63d Congress.]fl-r/fed-appFRA-LH-PL63-43.pdf

[H. R. 7837.]

An Act To provide for the establishment of Federal reserve banks, to furnish an elastic currency, to afford means of rediscounting commercial paper, to establish a more effective supervision of banking in the United States, and for other purposes.Be it enacted by the. Senate and House of Representatives of the United States of America in Congress assembled, That the short title of this Act shall be the "Federal Reserve Act."

Opening line. "An Act To provide for the establishment of Federal reserve banks, to furnish an elastic currency, to afford means of rediscounting commercial paper, to establish a more effective supervision of banking in the United States, and for other purposes."

fl-r/fed-appFRA-LH-PL63-43.pdfAn ”elastic currency” is a measure of what?

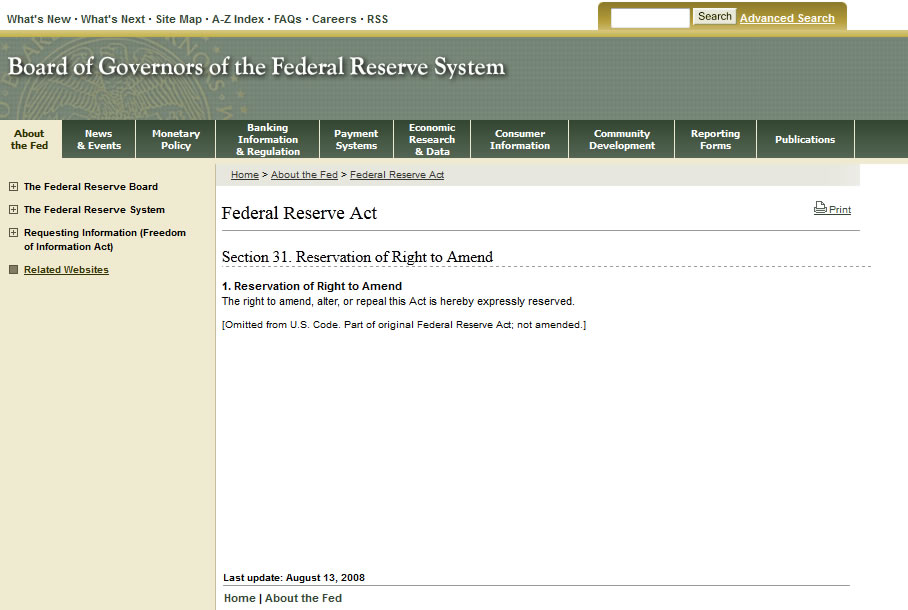

Federal Reserve Act Section 31. Reservation of Right to Amend

1. Reservation of Right to Amend

The right to amend, alter, or repeal this Act is hereby expressly reserved.

http://www.federalreserve.gov/aboutthefed/section31.htm

/images/fl-r/Fed-right-to-amend-sec31.PNG

The house of representatives represents the people, this is why they are elected directly and put in charge of the money. The senate represented the governments of the individual states, this is why they were initially appointed by and beholding to the state legislatures. So the check and balance of power was between the people's state governments and the people directly. This makes a bicameral legislature make sense.

The 17th amendment effectively dissolved the senate and removed the rights of the states. Senators are now nothing more than representatives that serve a longer term. The reason this was done was because controlling public opinion in order to manipulate the election of senators was easier than controlling all of the state legislatures.

The 16th and 17th ammendments were really not ratified. Knox, Secretary of State, 1913 "Deemed as Passed" the fraud into existence. Fraud. Extensive original, certified and notarized research is available at links provided below. This is in litigation now. Many mistakes were made all along the way; even after 97 years, few are corrected or punished, as usual.

National Archives, Seventeenth Amendment, Original Research

- How is it the ratification process could be "Deemed to Pass" by Knox?

- Devvy Kidd has the results from several people pulling records from 48 State archives. This case is in litigation for many years. When you read the file at the link, you will see many states voted on something quite different than the proposed amendment.

- "The Law that Never Was" website includes Income Tax, 16th and Senate, 17th Amendment Ratification Research

- A similar mess exists with the Income Tax,16th amendment.

2011 GAO Analysis

Summary

October 19, 2011 Federal Reserve Bank Governance: Opportunities Exist to Broaden Director Recruitment Efforts and Increase Transparency GAO-12-18

Highlights Page (PDF) Full Report (PDF, 127 pages) Recommendations (HTML)

Events surrounding the 2007 financial crisis raised questions about the governance of the 12 Federal Reserve Banks (Reserve Banks), particularly the boards of directors' roles in activities related to supervision and regulation. The Dodd-Frank Wall Street Reform and Consumer Protection Act required GAO to review the governance of the Reserve Banks. This report:

- (1) analyzes the level of diversity on the boards of directors and assesses the extent to which the process of identifying possible directors and appointing them results in diversity on the boards,

- (2) evaluates the effectiveness of policies and practices for identifying and managing conflicts of interest for Reserve Bank directors, and

- (3) compares Reserve Bank governance practices with the practices of selected organizations

The Federal Reserve Act requires each Reserve Bank to be governed by a nine-member board:

- three Class A directors elected by member banks to represent their interests,

- three Class B directors elected by member banks to represent the public, and

- three Class C directors that are appointed by the Federal Reserve Board to represent the public.

The diversity of Reserve Bank boards was limited from 2006 to 2010. For example, in 2006 minorities accounted for 13 of 108 director positions, and in 2010 they accounted for 15 of 108 director positions. Specifically, in 2010 Reserve Bank directors included 78 white men, 15 white women, 12 minority men, and 3 minority women.

According to the Federal Reserve Act, Class B and C directors are to be elected with due but not exclusive consideration to the interests of agriculture, commerce, industry, services, labor, and consumer representation. During this period, labor and consumer groups had less representation than other industries.

In 2010, 56 of the 91 directors that responded to GAO's survey had financial markets experience.

Reserve Banks generally review the current demographics of their boards and use a combination of personal networking and community outreach efforts to identify potential candidates for directors. Reserve Bank officials said that they generally limit their director search efforts to senior executives. GAO's analysis of Equal Employment Opportunity Commission data found that diversity among senior executives is generally limited. While some Reserve Banks recruit more broadly,

GAO recommends that the Federal Reserve Board encourage all Reserve Banks to consider ways to help enhance the economic and demographic diversity of perspectives on the boards, including by broadening their potential candidate pool.

The Federal Reserve System mitigates and manages the actual and potential conflicts of interest by, among other things, defining the directors' roles and responsibilities, monitoring adherence to conflict-of-interest policies, and establishing internal controls to identify and manage potential conflicts.

Reserve Bank directors are often affiliated with a variety of financial firms, nonprofits, and private and public companies. As the financial services industry evolves, more companies are becoming involved in financial services or interconnected with financial institutions. As a result, directors of all three classes can have ties to the financial sector. While these relationships may not give rise to actual conflicts of interest, they can create the appearance of a conflict as illustrated by the participation of director-affiliated institutions in the Federal Reserve System's emergency programs.

To increase transparency, GAO recommends that all Reserve Banks clearly document the directors' role in supervision and regulation activities in their bylaws.

One option for addressing directors' conflicts of interest is for the Reserve Bank to request a waiver from the Federal Reserve Board, which, according to officials, is rare. Most Reserve Banks do not have a process for formally requesting such waivers.

To strengthen governance practices and increase transparency, GAO recommends that the Reserve Banks develop and document a process for requesting conflict waivers for directors. The Federal Reserve System's governance practices are generally similar to those of selected central banks and comparable institutions such as BANK HOLDING COMPANIES companies and have similar selection procedures for directors. However, Reserve Bank governance practices tend to be less transparent than those of these institutions. For instance, comparable organizations make information on their BOARD COMMITTEES AND ETHICS POLICIES available on their websites; most Reserve banks do not.

Recommendations

Our recommendations from this work are listed below with a Contact for more information.

Status will change from "In process" to "Open," "Closed - implemented," or "Closed - not implemented" based on our follow up work.

Director: Orice Williams Brown williamso@gao.gov

Team: Government Accountability

Office: Financial Markets and Community Investment

Phone: (202) 512-5837

Orice Williams Brown

GAO Recommendations for Executive Action

Recommendation: While the Federal Reserve System recently has made changes to Reserve Bank governance, it can take additional steps to strengthen controls designed to manage conflicts of interest involving Reserve Bank directors and increase public disclosure of directors' roles and responsibilities. As such, to help enhance economic and demographic diversity and broaden perspectives among Reserve Bank directors who are elected to represent the public, the Chairman of the Federal Reserve Board should encourage all Reserve Banks to consider ways to broaden their pools of potential candidates for directors, such as including officers who are below the senior executive level at their organizations.

Agency Affected: Federal Reserve System

Status: In process

Comments: When we confirm what actions the agency has taken in response to this recommendation, we will provide updated information.

Recommendation: While the Federal Reserve System recently has made changes to Reserve Bank governance, it can take additional steps to strengthen controls designed to manage conflicts of interest involving Reserve Bank directors and increase public disclosure of directors' roles and responsibilities. As such, to further promote transparency, the Chairman of the Federal Reserve Board should direct all Reserve Banks to clearly document the roles and responsibilities of the directors, including restrictions on their involvement in supervision and regulation activities, in their bylaws.

Agency Affected: Federal Reserve System

Status: In process

Comments: When we confirm what actions the agency has taken in response to this recommendation, we will provide updated information. Recommendation: While the Federal Reserve System recently has made changes to Reserve Bank governance, it can take additional steps to strengthen controls designed to manage conflicts of interest involving Reserve Bank directors and increase public disclosure of directors' roles and responsibilities. As such, as part of the Federal Reserve System's continued focus on strengthening governance practices, the Chairman of the Federal Reserve Board should develop, document, and require all Reserve Banks to adopt a process for requesting waivers from the Federal Reserve Board director eligibility policy and ethics policy for directors. Further, consider requiring Reserve Banks to publicly disclose waivers that are granted to the extent disclosure would not violate a director's personal privacy.

Agency Affected: Federal Reserve System

Status: In process

Comments: When we confirm what actions the agency has taken in response to this recommendation, we will provide updated information. Recommendation: While the Federal Reserve System recently has made changes to Reserve Bank governance, it can take additional steps to strengthen controls designed to manage conflicts of interest involving Reserve Bank directors and increase public disclosure of directors' roles and responsibilities. As such, to enhance the transparency of Reserve Bank board governance, the Chairman of the Federal Reserve Board should direct the Reserve Banks to make key governance documents, such as such as board of director bylaws, committee charters and membership, and Federal Reserve Board director eligibility policy and ethics policy, available on their websites or otherwise easily accessible to the public.

Agency Affected: Federal Reserve System

Status: In process

Comments: When we confirm what actions the agency has taken in response to this recommendation, we will provide updated information.

2011 Federal Reserve Board Rife With Conflict of Interest, GAO Report (ABC):

http://publicintelligence.net

The makeup of the Federal Reserve's board of directors poses a conflict of interest and there is concern that several financial firms and corporations could have reaped monetary benefits from their executives' close ties to the Fed, according to a new report released today by the Government Accountability Office.

In one case, the Federal Reserve consulted with General Electric on the creation of a commercial paper funding facility and then provided $16 billion in financing to the company while its chief executive, Jeffrey Immelt, served as a director on the board of the Federal Reserve Bank of New York. Immelt is now President Obama's “jobs czar.”

JP Morgan Chase could also have benefited from its chief executive Jamie Dimon's position on the board of the Federal Reserve Bank of New York, according to the GAO. The bank received emergency loans from the Federal Reserve at the same time it served as the clearinghouse for the Fed's emergency lending program.

The Federal Reserve gave JP Morgan Chase an 18-month exemption from risk-based leverage and capital requirements in 2008, the same year that the Fed gave it $29 billion to acquire Bear Stearns, according to the GAO.

Similarly, Lehman Brothers' chief executive Richard Fuld served on the board of the Federal Reserve Bank of New York at the same time one of its subsidiaries participated in the Fed's emergency programs.

The Federal Reserve system has come under increased scrutiny in recent years, particularly for the structure of its board of directors. Executives of banks and companies that are regulated by the Fed, and that receive emergency funding from it, often serve on the board.

Federal Reserve Board Rife With Conflict of Interest, GAO Report

The makeup of the Federal Reserve's board of directors poses a conflict of interest and there is concern that several financial firms and corporations could have reaped monetary benefits from their executives' close ties to the Fed, according to a new report released today by the Government Accountability Office.

In one case, the Federal Reserve consulted with General Electric on the creation of a commercial paper funding facility and then provided $16 billion in financing to the company while its chief executive, Jeffrey Immelt, served as a director on the board of the Federal Reserve Bank of New York. Immelt is now President Obama's "jobs czar."

JP Morgan Chase could also have benefited from its chief executive Jamie Dimon's position on the board of the Federal Reserve Bank of New York, according to the GAO.

The bank received emergency loans from the Federal Reserve at the same time it served as the clearinghouse for the Fed's emergency lending program.

The Federal Reserve gave JP Morgan Chase an 18-month exemption from risk-based leverage and capital requirements in 2008, the same year that the Fed gave it $29 billion to acquire Bear Stearns, according to the GAO.

Similarly, Lehman Brothers' chief executive Richard Fuld served on the board of the Federal Reserve Bank of New York at the same time one of its subsidiaries participated in the Fed's emergency programs.

The Federal Reserve system has come under increased scrutiny in recent years, particularly for the structure of its board of directors. Executives of banks and companies that are regulated by the Fed, and that receive emergency funding from it, often serve on the board.

"Without more complete documentation of the directors" roles and responsibilities with regard to the supervision and regulation functions, as well as increased public disclosure on governance practices to enhance accountability and transparency, questions about Reserve Bank governance will remain," the report states, adding that such affiliations "could create reputational risk for the Reserve Banks."

The GAO did state that it "did not find evidence that Reserve Bank boards of directors participated directly in making any decisions about authorizing, setting the terms of, or approving a borrower's participation in the emergency programs." (THEY MUST NOT KNOW HOW TO LOOK)

The report also questions the independence of the Fed's own executives, some of whom have sought waivers for owning stock in companies that are regulated by the agency.

The Fed is not required to disclose those waivers.

In September 2008, Goldman Sachs received permission from the Fed to become a bank holding company and get access to loans from the Fed while Stephen Friedman, then chairman of the New York Federal Reserve's board of directors, owned shares in Goldman Sachs and sat on its board of directors. The Fed gave Friedman a waiver from its conflict of interest rules but did not consult with the board nor did it publicly disclose the affiliation.

One bank official told the GAO that the Fed gave the waiver because it would be difficult to find a chairman during a financial crisis and the bank already had one vacancy on its board. There was also concern that then-president Tim Geithner's possible nomination as treasury secretary would leave a major gap in the bank's leadership.

But the Federal Reserve was unaware that Friedman continued to purchase additional shares in Goldman Sachs, leading to his resignation in May 2009.

In a similar case, one director of the Federal Reserve Bank of Minneapolis was found to have shares in Merrill Lynch, which had been acquired by Bank of America, a bank that is regulated by the Federal Reserve.

Federal Reserve Chairman Ben Bernanke said in a letter to the GAO that the bank will consider ways to amend the bylaws to clearly explain the role of the directors.

New York Federal Reserve's president, William C. Dudley, recently acknowledged that such conflicts could tarnish the bank's image, and that it has taken steps to mitigate such issues. "We have to take appearance of conflict really seriously because it does affect the institution by creating questions about our credibility," he said.

Even the current makeup of the Federal Reserve Bank of New York's board of directors is especially corporate-heavy. It includes executives such as James Tisch, chief executive of Lowe's, and Terry Lundgren, chairman of Macy's.

"While these relationships may not give rise to actual conflicts of interest, they can create the appearance of a conflict as illustrated by the participation of director-affiliated institutions in the Federal Reserve System's emergency programs,' the report states.

"Most Reserve Banks" bylaws do not document the role of the board in supervision and regulation. To increase transparency, GAO recommends that all Reserve Banks clearly document the directors' role in supervision and regulation activities in their bylaws.'

The lack of diversity is also an issue, the GAO found. In 2010, only 15 of its 108 board of directors were minorities while a majority were white, senior executives of financial companies. At the same time, labor and union groups were disproportionately represented. In 2010, 56 of the 91 directors that responded to GAO's survey had financial markets experience.

The report comes as the Occupy Wall Street movement rallying against Wall Street and corporate greed is gaining momentum. Some politicians, such 2012 Republican presidential candidate Rep. Ron Paul, R-Texas, are also raising calls to end the Federal Reserve or scale back its role.

1993 Federal Reserve System Audit

Federal Reserve System Audits: Restrictions on GAO's Access T-GGD-94-44 October 27, 1993

Full Report (PDF, 16 pages) Recommendations (HTML)

Summary

Currently, GAO lacks audit authority over the Federal Reserve's monetary policy, foreign transactions, and Federal Open Market Committee operations. Legislation pending before Congress would remove all restrictions on GAO's authority to examine Federal Reserve activities. Although whether to expand GAO's authority is clearly Congress' call, GAO believes that if its authority is expanded, measures should be included to protect against release of confidential documents and to prevent undue interference with the Federal Reserve's ongoing policymaking functions.

Director: Orice M. Williams

Team: Government Accountability Office: Financial Markets and Community Investment

Phone: (202) 512-8678

Matters for Congressional Consideration

Recommendation: If Congress decides to remove the existing restrictions on GAO audit authority, it should include certain safeguards in the legislation. These safeguards, which are similar to those that already exist under GAO present authority, should: (1) prohibit GAO from disclosing the identity of foreign central banks or governments; (2) prohibit GAO from disclosing confidential documents and requires safekeeping of confidential information; and (3) specify delays

Status: Open

Comments: GAO believes that this recommendation will remain valid and should be considered as part of any future congressional oversight of the Federa Reserve System.

1964 House Banking Committee vs. federal reserve

Banking: Fight over the Federal Reserve

Friday, Feb. 14, 1964

In a Washington hearing last week, the chairman of the House Banking Committee stared at one of the nation's top managers of money. Grumbled Texas Representative Wright Patman: "You can absolutely veto everything the President does. You have the power to veto what the Congress does, and the fact is that you have done it. You are going too far."

The object of Patman's wrath was ascetic-looking Alfred Hayes, president of the New York Federal Reserve Bank and a ranking member of the U.S.'s powerful central banking system. For three decades, Wright Patman has fumed and fussed that the Federal Reserve System is too secretive, too independent, too insensitive to the hopes of small borrowers. A sharecropper's son, he often charges that it is a tool of Wall Street bankers.

Immediately after moving up to the chairmanship of the Banking Committee last year, Patman started preparing what has become one of the farthest reaching investigations in the Federal Reserve's 50-year history. Patman has a team of economists and consultants studying the system with a critical eye, intends to call twelve top non-Government economists to the stand by month's end, and is pressing for new legislation to curb the central bank.

Expansion or Stability? The controversy comes at a pivotal time. Calmer critics than Patman accuse the Federal Reserve of starting, or at least contributing to, the recessions of 1958 and 1960 by hiking interest rates and reducing the credit supply in its zeal to head off inflation. Now that some prices are rising anew, the central bankers again must ponder the question of whether to battle inflation at the risk of nipping the economy's three-year-old expansion. In recent months Chairman William McChesney Martin Jr. who occupies what Patman somewhat extravagantly calls "the most powerful job in the civilized world" successfully campaigned for a slight squeezing of credit and rise in interest rates. But his colleagues are sharply divided on the issue, and the Federal Reserve is being pelted with criticism from several sides.

Treasury Secretary Douglas Dillon, Presidential Economist Walter Heller and M.I.T. Economist Paul Samuelson lately have taken up the argument that Martin and his colleagues unwisely tightened money before the last recession.

Attacking the system's penchant for secrecy, such Democrats as Wisconsin Senator William Proxmire complain that trying to find out why and how the Federal Reserve makes its decisions is like "trying to paste a custard pie on a wall."

To make the Federal Reserve more dependent upon the President and upon Congress' easy-money advocates, Patman is sponsoring bills that would:

- End its authority to set its own budget (currently: $180 million a year) and oblige it to come to Congress for an annual appropriation.

- Empower the General Accounting Office to audit its books. Expand its board of governors from seven to twelve, with the chairman to be the Secretary of the Treasury.

- Eliminate its credit-regulating Open Market Committee and transfer the committee's powers to the expanded board.

At least four members of this board would be new presidential appointees, and they presumably would be amenable to the wishes of Congress and the President.

What Will Johnson Do? Chairman Martin admits that the Reserve has made mistakes and could stand some reforms.

( See The Purpose of the Senate )

But he champions its freedom to make unpopular decisions, and argues that its unique strength has been in keeping control of the money supply out of the hands of politicians.

He fears that Congress would be tempted to tamper with policy if it had power over the system's purse, and that the Treasury Secretary would be subject to a conflict of interest if he also headed the Federal Reserve. Says Martin: "The question is whether the principal officer in charge of paying the Government's bills should be entrusted also with the power to create the money to pay them."

Many businessmen and bankers, who consider Martin the very symbol of sound money, will lobby against attempts to rob him of authority or to pack the board.

But Patman senses a widespread feeling that the whole Federal Reserve needs an overhaul, and he is confident of bucking through at least a few of his proposals. Much will depend upon whether his fellow Texan in the White House decides to press hard for the changes. Lyndon Johnson shares Patman's Populist dislike of tight credit, and is not as close to Bill Martin as John Kennedy was. The tip-off as to where he stands in the fight may come when he selects a man to fill a current vacancy on the Federal Reserve Board. The President's decision is long overdue, and so far he has not told even Bill Martin what kind of a man he will pick.

Board of Governors of the Federal Reserve System Washington D.C.

2/25/1958 Correspondence to the Board Z-4592

Enclosed is a preliminary copy (page proof) of Representative Patman*s statement during the hearings before the House Banking and Currency Committee

Mr. PATMAN. There is no decision holding that (he statute was valid.

The CTIAIHMAN. 1 want you to understand 1 am not making any arguments that the banks should go into the insurance business. That, has nothing to do with it.

Mr. BATMAN. YOU are supporting this bill; that insurance section is not in the law, and you are trying to put it in. You are trying to put the banks in the insurance business, Mr. Chairman. You cannot get around that.

The CHAIRMAN. T am only thinking about, what., considered to what, was in the law. It only applied to towns of less than 5,000 people.

Mr. BATMAN.* My time is limited and J do not care to go into that point any further. The Chairman will never be able to show a decision where the courts have passed upon the validity of the statute.

Now as to the Federal Reserve System:

PAY OFF THE SO-CALLED STOCK* OF THE FEDERAL RESERVE BANKS

Now some of the bankers who have appeared before our committee, here revealed that they have been under an impression that the Federal Reserve banks are owned by the commercial banks, the member banks.

Yesterday, I made a speech on the floor, in which I referred to this erroneous impression, and in which I showed conclusively that the Federal Reserve banks are owned by the Government of the United States. Tliere is no valid, legal stock held by commercial banks in the Federal Reserve banks. That so-called stock that the member banks own is not stock at all; "stock" is a misnomer. It has no stock value; it cannot be voted as stock; it cannot be sold; it cannot be hypothecated; it is just held as an investment or a loan upon winch they draw G percent. The banks do not own the Federal Reserve System.

Tins 6 percent interest which amounts to about $20 million a year should certainly be saved by the Government, by canceling that stock and paying it off. It could easily be paid out of the Federal Reserve surplus funds, now, without any inconvenience.

MAKE THE FEDERAL RESERVE BOARD" THE OPEN MARKET COMMITTEE

I am going to offer an amendment, Mr. Chairman, to increase the Federal Reserve Board to 12 members, and make it the Open Market Committee.

I have had a bill of this kind pending for a number of years. We have never had.a hearing on the bill, but I am going to offer it as an amendment to these bills.

Wejknow that operations of the Open Market Committee are in the New York bank alone. The Open Market Committee delegates to one man, who is in charge of the open market account, responsibility for carrying on trading with private brokers, amounting-to tens of billions of dollars worth of securities. There are dozens of people who know about the operations of this important comn ittee. With knowledge of what their account is going to do, a person can make millions overnight. We ought to look into that and find out what is going on. pg.7

I asked the gentleman who was president of the New York Reserve Bank just before Mr. Hayes, Mr. Sproul if it had any rules against bank officials or employees playing the market. He said no, except they couldn't buy on margin.

Now, imagine that. Here is a bank that is run bv private bankers in New York, handling Government bonds and other securities aggregating tens of billions of dollars a year, and we have never inquired into the procedures that they use. We have never attempted to determine whether or not it was being honestly conducted.

There are 17 dealers that trade with the open market account. I wouldn't say that they are handpicked but there are very few, usually about 12. In 1956, only 5 of these accounted for over 50 pei'cent of all the transactions of the open market account.

To show you something about the size of the operations, in 1956 the open market account purchased $11.9 billion worth of Government securities and sold $9.3 billion worth. Total transactions, $21-.2 billion during that 1 year alone. So it is not a small matter; this is not small potatoes. Twenty-two billion dollars worth of securities bought and sold in 1 year. I wouldn^t consider that an extraordinary year; they do about that much almost every year. And yet we have never looked into their operations; they have never been audited by the General Accounting Office; and we know almost nothing about them.

But I can tell you this much,because I have made inquiries; this so-called Open Market Committee operates the biggest market in the wrorld; and while it is called an "open market*" it is the most closed market that was ever invented. The people who operate this account do the buying-and-selling of Government securities, using Government money, and decide for themselves what price they will takg or pay, in each trade; they decide which one of their little select group ot dealers they will sell to pi* buy from; and there is never any public announcement of the prices this account pays or receives; there is never any public record of how much securities they sell to or buy from any one of their select group of dealers; and the people who carry on this under-the-counter trading in tens of billions of dollars each year of Government-owned securities are not even Government employees.

More than that, Chairman Martin refuses to tell the public, or even to tell this committee in confidence, anything about these dealers who are privileged to carry on this fabulous and hidden trading with the open market account. Chairman Martin has told us their names, and that is about all. He has refused to tell us what their net worth is and what percentage of the Government securities they hold at any one time, and he has refused any information about how much trading in Government securities these dealers do with their custdomers-.

I will insert a table showing the monthly volume of purchases and sales in 1954, which was a $11.6 billion year. This table shows that the open market account outright sales of securities amounts to $3.3 billion. We can assume that most of these outright sales were made to dealers, as contrasted to foreign control banks. At the same time the open market account made loans, that is, repurchase agreements, with the dealers amounting to $2.4 billion,

pg.8

You see, the Open Market Committee conceives of this little group of dealers as being "the makers of primary markets" for Government securities. In plain words, the open market account conceives of itself as adjusting from day to day the amount of money in the private banking system of the country. When there is too much money, according to the account's opinion, they buy some money in from these dealers and pay the dealers a profit on it; and ,when they think there is too little money, they sell some to these dealers and, of course, the dealers get their wholesaler's margin on this as they resell the securities to the banks, the corporations, or anyone else who may want to buy them.

Hundreds of member banks all over the country buY and sell Government securities, but they must go to the dealers for these. For mysterious reasons which have never been explained, they never trade directly with the open market account.

The open market account does trade with foreign central banks, they buy and sell billions of dollars worth of United States Government securities, all over Europe, all over South America, and everywhere else that there is a foreign bank that wants to trade with the open market account.

In contrast, however, the Federal Reserve banks themselves cannot trade with the open market account. These banks act as agents for the member banks and others ip buying and selling billions of dollars worth of Government securities but the Federal Reserve banks must also go to the dealers to trade, or go to some subsidiary dealers who in turn trade with the top dealers that the open market account trades with. Considering the vast amount of trading that is going on at almost all times, it is inevitable that there are many times when the Federal Reserve banks are in the market buying securities from private dealers at the very moment the open market account is selling those same securities to private dealers. And of course the sale by the open market account is on behalf of the Federal Reserve banks.

Under the 1913 act, each Federal Reserve Bank had its own opeN market committee, but the 1935 act completely clumped the Federal Reserve System. There is now only one Open Market Committee, and the Federal Reserve Bank of New York is the sole agent of that committee. This bank handles the entire account, and although it is supposed to operate according to policy guides laid down by the Open Market Committee, if you will read these policy guides -which are published in the Annual Report of the Board you will find that they are vague statements which leave the actual decisions up to the New York bank.

If you turn to the Annual Report of the Board of Governors, for instance say 1956 you will see that the Dallas bank

1 happen to be in the Dallas district -that the Dallas bank earned from discounts and advances only $850,142. That is all that whole bank earned. Of course, it has earnings in its statement of $23 million. Where did the other come from? It comes directly from New York. None of these other 11 banks touches those Government securities in the open market. They are all right there in the city of New York in the Federal Reserve Bank Building. The coupons a;re clipped there, the interest is collected there, the taxpayers pay it into the treasury and the treasury sends it up to the Federal Reserve Bank of New York, to pay interest on over $23 billion of government bonds that have been bought by that open market account and which they now hold. The New York bank then sends to Dallas, Texas, $22 million, as the Dallas bank's part of the earnings. Did they earn that? They didn't turn their hands to get it.

The open market account bought these bonds on the credit of the Nation, using Federal Reserve notes which are also Government obligations; then the New York bank sends the money to Dallas, to San Francisco, Kansas City, Minneapolis, Chicago, Atlanta, Richmond, Cleveland, Philadelphia, New York, and Boston. Each one their proportionate share, but the, banks don't touch these bonds. They render no service for this income, and the bonds were purchased on Government credit.

The Dallas bank, although it only earned $830,000, it spent more than $6 million--$6,080,000.

Now this operation in 1935, on the Federal Reserve banking system, changed it completely, from an autonomous regional system to a central banking system.

We now have a central bank in the United States, and under this central banking system, there is no important power left in the regional banks. There is no important power left; It is all done by the Federal Reserve Board here in Washington or by the Open Market Committee composed of 12 members, all of whom are selected by representatives of private banks.

When the Open Market Committee meets, there are 12 members of private banks there at the meeting, presidents of the Reserve banks. Only five of these can vote but the others are there to participate in the meetings and to help evaluate tin4 problems and to help come to decisions. Those 7 public, members the Board members--are surrounded not only by these 12 representatives of the private banks but I hey have 12 other people with whom they must deal who directly represent the banks, too. These-are known as the Federal Advisory Council. So we have our 7 public members surrounded by 24 bankers to help them perform their public services and public, duty.

I say that alone should arouse our thinking. We should look into this carefully and make sure that it is being done in the public interest, and in the meantime we know that we should take the bankers off of the Open 'Market Committee. pg 10

agreement. I said awhile ago, I don't see anything in the law authorizing this.

Under this practice that has been built up, because nobody has been looking over their shoulder or auditing their books, these Federal Reserve people have been going foot-loose and fancy-free. That practice of lending the dealers money to carry Government securities is one that certainly should receive some attention.

THE DISCOUNT RATE SHOULD BE FIXED BY THE BOARD NOT PRIVATE, BANKERS

I am also going to offer an amendment to require that the Board of Governors and the Board alone fix the discount rates. As we know, when a change in the Federal Reserve discount rate is announced, securities markets shoot up or down, just in a matter of minutes. Values of stocks, Government bonds, and all other securities change by billions of dollars.

Now, Mr. Chairman, we have in our own Federal Reserve System the same procedure for changing the discount rate that they have in the Bank of England. The boards of directors of the Federal Reserve banks recommend a change and these boards are made up of private bankers and men who are also on the boards of the big corporations. This procedure is open to exactly the same problem that has recently come up in connection with the Bank of England. There they have some of the directors of the Bank of England, their central bank, who are also bankers; and they have some who are on the boards of industrial corporations.

They are very quick to point out that not one of the six largest banks in England is allowed to have representation on the board of the Bank of England. None of the big banks is allowed representation on that board. But some of the smaller banks are.

Recently it was shown that where the Bank of England was going to raise the discount rate from 5 to 7 percent, one of the bank's directors who had recommended the change advised his corporation to unload its holdings of "guilt edge" bonds "which the corporation did to the extent of $2.8 million worth" the day before the change in discount rate was publicly announced. Later, when this matter came to light during an investigation, the director in question, a Mr. Keswick, testified quite frankly that, he felt he owed equal loyalties to the bank and to his corporation. A Renter's dispatch of December 6 reported: "William J. Keswick said that as a director of the bank, he could not betray secrets, and yet he was bound to protect the business interests he legally represented." pg 11

THE FEDERAL RESERVE SYSTEM SHOULD CARRY ITS OWN INSURANCE

Now, the Federal Reserve banks are buying insurance of all kinds. They are spending over $1 million a year; $1,821,429 during the year 1950 for insurance:

Why should the Federal Reserve banks buy insurance?

Whom do they buy it from? Who gets the commissions? Are they connected with the banks? We don't know. This insurance is unneeded, it is, unnecessary. These Reserve banks are part of the Government just as much so as the Capitol. And with all the money and resources of the Federal Reserve System, if it cannot carry the risk of its own insurance, then certainly there is no private insurance company that can carry this risk.

Suppose someone suggested that the Congress should take insurance on the Capitol storm insurance, hail insurance, rain insurance, cyclone insurance for which-the Government would be charged a fee. We would certainly not.like that.

Well, this is a comparable situation. The Federal Reserve banks are doing just that. Why are they allowed to do it? It is because they have never been looked into. Their books are never audited. They are never audited and never have any supervision. That matter should certainly receive the attention of this committee.

THE FEDERAL RESERVE SYSTEM MUST BE SUBJECT TO AUDIT

Another amendment I will offer to the Federal Reserve Act portion of these bills will require that the Federal Reserve Board, the Federal Reserve banks, and the Open Market Committee be audited by the General Accounting Office.

Since its organization in 1913, there has never been an outside audit of the System or any part of it.

Now this is shocking, Mr. Chairman. It is bound to be shocking to all American citizens that we would let the Federal Reserve System handle hundreds of billions of dollars of the Government's money and two-thirds of every board of directors of each Federal Reserve bank is composed of private bankers or people selected by the private bankers and never have any audit.

The only audit Federal Reserve banks have ever had is an internal audit, where they select the auditors, give the auditors their instructions, and report back to themselves. It is bordering on a disgrace for Congress to permit that situation to continue. It just doesn't make souse, either common, book or horse. There is just no sense to it.

I will come back to this point later, and give the committee some illustrations taken from their own internal audit reports which will, I think, give convincing proof of the need for having the. Reserve banks audited. pg.13

The Comptroller of the Federal Reserve System Are Not Audited

Now, the General Accounting Office has never audited the books of a Federal Reserve bank, Federal Reserve Board, or the Comptroller of the Currency, Mr. Chairman.

The office of the Comptroller of the Currency has handled over $154 billion worth of Federal Reserve notes; it has received this much from the Bureau of Printing and Engraving; it has issued a major percentage of this to the Federal Reserve banks; it has received back a large percentage of this for destruction; and it holds several billion dollars worth in custody, yet none of h.ese operations is subject to any audit; they are not even audited by the Treasury's own internal auditors.

The Federal reserve system, as 1 have pointed out, lias never had a Government audit. It has never had any audit by independent auditors from outside Ihe system itself. There are internal audits, made by personnel of the system, and even these audits taking them for what they are, internal audits show on their face to be subject to serious inadequacies and limitations. The audit teams are supposed to be made up so that the employees of one bank audit another bank, but even this principle is rarely followed 100 percent. In practice the employees of a particular bank are on the team to help audit their . own banks.

These internal audits of the Federal Reserve banks have many limitations with respect to verification of currency, checks, <i'old, and securities. Frequently the banks' audits do not conform to the recommended procedures of the Conference of Auditors and the audit committees of the boards of directors of the banks themselves. The audit committees override the recommended procedures of the Conference of Auditors. Sometimes audit committees of the board of directors fail to meet even once a year. Examples

pg 49

Now, if there ever was a disgrace, it is Congress' permitting people to have complete control of United States currency who do not consider themselves obligated to the Government, at least not even a Government employee. Some of these employees of Federal Reserve banks are, but they are not willing to admit it, and they do not concede it.They claim they are not.

They have charge of destroying the worn and mutilated currency. And, of all the irregularities and seemingly dishonest dealings in connection with it, you will find plenty of eye openers in these reports that even their own auditors made about the irregularities in handling the tremendous amount of money that is destroyed 'every year, and the loose fashion in which it is handled.

Up at Pittsburgh, a cyclone or a heavy wind hit the city while currency was being destroyed in the municipal incinerator and scattered money all over Pittsburgh, Pa. The only reason we found out about it through the newspapers and they had to redeem a lot of that currency because it wasn't bunted and under certain conditions it is redeemable.

There are other cases just as bad as that throughout the United States.

In July of 1953, the Federal Reserve banks took over the destruction of unfit United States currency which had previously boon handled by the Treasury Department. The principal reason given for the changeover was to save the expense of transporting the currency back to Washington for destruction the only possible savings since the Treasury reimburses the banks for the actual costs of destruction. However, one expense not considered was the costs to the Federal Reserve banks and branches for the installation of incinerators and other equipment' for destruction. These costs the Federal Reserve banks have charged off to current expenses, thereby reducing their revenues and amount of money paid into the Treasury by the Federal Reserve. And the savings to the Government, if there have been any, have been at the sacrifice of less security over United States currency.

The banks have destroyed around $8 billion of currency since 1953 and this without Government audit.

The banks have employed inadequate controls over the destruction of United States currency. Although their own auditors recommended methods of improving procedures, the same weaknesses continued throughout the System year after year.

Banks permit canceled currency to be destroyed by the same em ployees who act as verifiers, contrary to Treasury regulations.

They do not verify bundles not included in percentage counts nor do they make any determination that the standard of fitness of the currency conforms to Treasury regulations.

pg 70 I can state, however, that according, to one report of the T)pen Market Committee that I have seen, the open-market account ho ugh t from and sold to lo of these dealers who are not hanks that is, nonbank dealers

Who are these dealers? We have their names and that is about all. I will list these names and then point out what 1 have tried to do to learn something for myself about who these dealers are.

Dealer:

Discount Corp

Chemical Corn Exchange Bank

Salomon Bros. & Hutzler

C. J. Devine & Co

Aubrev G. Lanston & Co., Inc

D. W/Rich & Co :

C. F. Childs & Co., Inc

Guaranty Trust Co

Rankers Trust Co

First Boston Corp

Continental Illinois National Bank & Trust Co., Chicago

Hriggs, Schaedle & Co., Inc r

First National Bank, Chicago

Win. E. Pollock & Co., Inc

N. Y. Hanseatic Corp

J. G. White

Chas. E. Quincey & Co

Now, I think the committee should look into the Open Market Committee and try to find out a little something about who these, dealers are that serve as the funnels through which our great Federal Reserve System passes out additions to the money supply of the country, and pulls in substructions from the money supply of the country. So, I have had the first 10 names looked up - that is the names of the 10 biggest dealers- to try to find out who the people are that are partners in these dealer firms, and who are the officers and directors in these dealer firms where the firm is incorporated.

I have asked for information on the other connections of these people wherever such information is available from published directories Well a huge percentage of these people do not publish information about themselves. But enough of them do give information to show us that they represent all of the big money interest of the country, the big commercial banks, the big investment banks, the big insurance companies, the trust funds, and the big industrial and utility corporations.

The following list shows the names of the top officials in each of the 10 dealer firms doing the largest volume of business with the open-market account in 1956. Then, where information is published about the other connections of the individuals, those, connections are shown too.

Guaranty Trust Co., New York

Cleveland, J. Luther, chairman and director

Guaranty Safe Deposit .Co., director

Atchison. Topeka <fe Santa, Fe Railway, director

Anaconda Co., director

Discount Corporation of New York, director

Sunray Mid-Continent Oil Co., director

Kleitz, William L., president and director

Wilson & Co., director

IBM World Trade Corp., director

Liverpool & London & Globe Insurance Co., Ltd., member local board in NewYork

Royal Insurance Co., Ltd., member local board New York

British & Foreign Marines Insurance Co., Ltd., member local board in New York

Virginia Fire & Marine Insurance Co., director

Thames <v. Mersev Marine Insurance Co., Ltd., member local board in T New York

Newark Insurance Co., director

Queen Insurance Company of America, director

American & Foreign Insurance Co., director

Globe lndemnity Co.. director

Royal Indemnity Co.. director

Star Insurance Company of America, director

One Hundred Fifty William Street Corp., director

W. T. Gran Co., director

American Smelting & Refining Co., director

Sharp, Dale E., executive vice president

Standard Accident Insurance^ Co., director

Pilot Insurance Co. (Toronto), director

Planet. Insurance Co., director

Yorkshire Insurance Company of New York, chairman

Seaboard Fire & Marine Insurance Co., director

Jerman, Thnomas Palmer, executvie vice president

Union Pacific Railroad, director

Broome, Robert E., vice president

Iowas Public Service Co. director

Town Public Service Co., director

McCabe, Herbert P., vice president

New Jersey Natural Gas Co.. director

Palmer, Louis Babcoek, vice president

Peerless Insurance Co., director Verbeck, Cuido F., Jr., vice president

Morris County Savings Bank, director Wallace. John Brougham. Jr., vice president

Union Terminal'Cold Storage Co., director

Manhattan Refrigerat ing Co.. director

Interwoven Stocking Co.. director ,

White, William RafTord, vice presidc.nl

Bowery Savings Bank, trustee, member executive committee Strelow, William Richard, \ ire president

Pan American Society of United States, director.

National Council American Importers, Inc., director

National Foreign Trade Council, director

pg. 92 Federal Reserve System Personnel who are directors and officers of major Financial Companies

Philadelphia + Financial + Institutions and more

Secrets of

The Power Elite Since 1833

The Russell Trust Association was first established among the class graduating from Yale in 1833. Its founder was William Huntington Russell of Middletown, Connecticut. The Russell family was the master of incalculable wealth derived from the largest U.S. criminal organization of the nineteenth century: Russell and Company, the great opium syndicate.

1st of all you need to know that George Walbridge Perkins, Sr. is a direct descendant of the opium drug smuggler Perkins family. The founding families of Skull & Bones included the Russell and Perkins families, Over several generations, however, all these families heavily intemarried and became, in effect, one extended power grouping. They considered themselves to be a special among the merchant, banking, and Puritan Pilgrim elite of Yale. They took the Puritan beliefs of the early New England settlers, that they were "elected by God," and pre-ordained to rule North America.

J. P. Morgan incorporates United States Steel as the first billion-dollar company. He partners with George Walbridge Perkins, Sr. In 1912 he helped organize Theodore Roosevelt's new Progressive party, becoming its executive secretary. At the convention an anti-trust plank was suddenly dropped, shocking reformers like Gifford Pinchot who saw Roosevelt as a true trust-buster. They blamed Perkins (who was still on the board of U.S. Steel and remained on it until his death.)

McKinley is assassinated and Theodore Roosevelt becomes president.

1907

USA

The "Panic of 1907" begins with a run on Knickerbocker Trust Company stock October 22nd sets events in motion that will lead to a depression in the United States. The recession would last until 1908.

"All this trouble could be averted if we appointed a committee of six or seven men like J. P. Morgan to handle the affairs of our country." — Woodrow Wilson

(Sir William Wiseman, tenth baronet of Ulster, partner in Manhattan's Kuhn, Loeb & Co., was the second most powerful Briton in the U.S., unofficial head of His Majesty's World War I secret service in the U.S. and Woodrow Wilson's "confidential Englishman." Sir William Wiseman, "the chief British spy master in America during World War I," was a Kuhn, Loeb partner and advisor to John Schiff, grandson of Jacob Schiff and the chief partner. (The Warburgs, by Ron Chernow. Random House, 1993, pp 612-613.) He was a correspondent of Strauss between 1941 and 1962.

"Those not favorable to the money trust could be squeezed out of business and the people frightened into demanding changes in the banking and currency laws which the Money Trust would frame." — Rep. Charles A. Lindbergh (R-MN)

1908

USA

The Glass-Owen Act was passed in response to the Panic of 1907. Its purpose was to provide for the issue of emergency currency during widespread financial crisis. The National Monetary Commission was also established under this act to develop a more durable solution to the nation's problematic financial and banking practices.

The Financial Purpose of the Senate explained in 1906 by David Graham Phillips

The Treason of the Senate: Aldrich, The Head of It All by David Graham Phillips Cosmopolitan March 1906

1909

The Russell Building was occupied in 1909 by the Senate of the 61st Congress.

Introduction to The Russell Family and the Russell Trust Association.

Skull and Bones, a secret society founded in 1832 at Yale University in New Haven, Connecticut.

Founding members (1832-1833 academic year) Opium Drug Smuggling Pirate William Huntington Russell (1833), Connecticut State Legislator, Major General descendent.

Jekyll Island

and the

Federal Reserve

1908-1912: The Stage is Set for a Decentralized Central Bank

- The Aldrich-Vreeland Act of 1908, passed as an immediate response to the panic of 1907, provided for emergency currency issues during crises. It also established the National Monetary Commission to search for a long-term solution to the nation's banking and financial problems. Under the leadership of Sen. Nelson Aldrich, the commission developed a banker-controlled plan.

- William Jennings Bryan and other progressives fiercely attacked the plan; they wanted a central bank under public, not banker, control. The 1912 election of Democrat Woodrow Wilson killed the Republican Aldrich plan, but the stage was set for the emergence of a decentralized central bank.

1912: Woodrow Wilson as Financial Reformer

Though not personally knowledgeable about banking and financial issues,Woodrow Wilson solicited expert advice from Virginia Rep. Carter Glass, soon to become the chairman of the House Committee on Banking and Finance, and from the Committee's expert adviser, H. Parker Willis, formerly a professor of economics at Washington and Lee University.Throughout most of 1912 Glass and Willis labored over a central bank proposal, and by December 1912 they presented Wilson with what would become, with some modifications, the Federal Reserve Act.

1913: The Federal Reserve System

is Born

1913: The Federal Reserve System is Born

From December 1912 to December 1913 the Glass-Willis proposal was hotly debated, molded and reshaped. By December 23, 1913, when President Woodrow Wilson signed the Federal Reserve Act into law, it stood as a classic example of compromise—a decentralized central bank that balanced the competing interests of private banks and populist sentiment.

The Federal Reserve System was created by the Federal Reserve Act and signed into law by President Woodrow Wilson on December 23, 1913. Although the Act was passed in the final days of the legislative session, it had been debated for some time in earlier versions.

Because the regional Federal Reserve Banks are privately owned, and most of their directors are chosen by their stockholders, it is common to hear that control of the Fed is in the hands of elite bankers. However, individuals do not own stock in Federal Reserve Banks. The stock is held only by banks that are members of the system. Ownership and membership are synonymous.

QUESTION: Why is the Fed sometimes called a decentralized central bank that's both public and private?

OFFICIAL ANSWER

The Federal Reserve consists of two main entities—the Board of Governors and the 12 Federal Reserve Banks. The Board of Governors is a public agency.The 12 Federal Reserve Banks and their boards of directors represent the private component of the Fed.

REAL ANSWER:

Contrary to popular belief, the world's finances are controlled by privately-owned “central banks” masquerading as federal government banks in nearly every country in the world.

The U.S. Court of Appeals, Ninth Circuit, ruled that The Federal Reserve (U.S.' central bank) was privately owned in 680 F.2d 1239, LEWIS v. UNITED STATES of America, No. 80-5905. http://land.netonecom.net/tlp/ref/federal_reserve.shtml

The 12 Federal Reserve Banks and their Boards of Directors represent the private "SPECIAL INTERESTS" OF private families who control the Boards of Directors.

WHICH PRIVATE BANKS OWN SHARES OF THE FEDERAL RESERVE

NOTE THE FOLLOWING FAMILIES from the antisemit Bigot Col. James "Bo" Gritz, the 1992 Presidential candidate of the extremist Populist Party, charged that "eight Jewish families control the FED" (Federal Reserve System) in a book Called to Serve.

Brothers & Co., Bankers

Southeast Corner Fourth and Chestnut Sts. Philadelpha PA

"Founded in 1798. Deal in exchange; issue letters of credit; make high-grade investments; negotiate loans; receive deposits and transact a general banking business."

Also know about Brown, Shipley & Co. History of the Atlantic Cable & Undersea Communications from the first submarine cable of 1850 to the worldwide fiber optic network.

For more information on the Brown family and their banking enterprises, see this PDF document on the 1901 Brown building in Baltimore, produced by the US Government’s Historic American Buildings Survey, which includes a detailed history of the company.

CONNECTICUT SECRETS

In 1943, by special act of the Connecticut state legislature, its trustees were granted an exemption from filing corporate reports with the Secretary of State, which is normally a requirement.

"From 1978 onward, business of the Russell Trust Association was handled by its single trustee, Brown Brothers Harriman & Co. partner John B. Madden. Madden started with Brown Brothers Harriman in 1946, under senior partner Prescott Bush. Father of both Presidents named BUSH

1) http://www.dailymotion.com/video/x3pjco_hear-a-traitor-speak-1of2_news

2) http://www.dailymotion.com/video/x3pjg3_hear-a-traitor-speak-2of2_news

Jeykill Island - JP Morgan

Senator Nelson Aldrich -- Banking Family Exposed

Jacob Schiff

It is done this way in England. Who Owns the Bank of England

1913

USA

The Federal Reserve Act, also known at the time as the Currency Bill, or the Owen-Glass Act. The bill called for a system of eight to twelve regional Reserve Banks that would be owned by commercial banks and whose actions would be coordinated by a committee appointed by the President. The Federal Reserve System would be a privately owned central banking system. Bankers would run the twelve Banks and those Banks would be supervised and by the Federal Reserve Board.

Official Version

The Federal Reserve Act was passed of December 23 by a vote of 298 to 60. The Senate passed the measure 43 to 25. President Wilson signed the bill on December 23 at 6 PM.Unofficial Version

The bill had been shepherded through a Congressional Conference Committee meeting scheduled for between 1:30 - 4:30 AM (when most members of Congress were asleep) on December 22, 1913. The Act was then voted on the next day and passed although many members of the body had left for the Christmas holidays and most others who stayed behind hadn't had time to read it or know its contents.

see

Colonel

Edward Mandell House

pdf

# Thomas N. Perkins 36th Generation of the Skull and Bones Opium Drug Smuggling Perkins Family

"In 1913, Colonel Edward Mandell House helped to pick the charter members of the original Federal Reserve Board.

Edward Mandell House (originally Huis). He was close to the US Morgan banking dynasty.

He convinced the Morgan group, and the media to support Wilson. This financial support helped Wilson win the election. He worked behind the scenes advising and controlling politicians who are said to be easily purchased and discarded. He was one of the most powerful men in American politics, and yet remains unknown to most Americans, because he worked in the shadows.

Edward Mandell House wrote Philip Dru: Administrator

The free ebook version is approximately 131 pages and 53 chapters. At the end of the book there is a four-page article entitled “What Co-Partnership Can Do” written by the Governor General of Canada, Earl Grey (Served from 1904-1911)

Without realizing it, every American will insure us for any loss we may incur and in this manner, every American will unknowingly be our servant, however begrudgingly. The people will become helpless and without any hope for their redemption and, we will employ the high office of the President of our dummy corporation to foment this plot against America.”

"The Intimate Papers of Colonel House":

In 1913, Colonel Edward Mandell House helped to pick the charter members of the original Federal Reserve Board. Edward Mandell House (originally “Huis” which became “House”) was born July 26, 1858 in Houston, Texas. He became active in Texas politics and served as an advisor to President Woodrow Wilson, particularly in the area of foreign affairs. House functioned as Wilson's chief negotiator in Europe during the negotiations for peace (1917-1919), and as chief deputy for Wilson at the Paris Peace Conference. He died on March 28, 1938 in New York City.

Edward and his father had friends in the Ku Klux Klan. The Klan dispensed vigilante justice after the Civil War. In 1880 a new legitimate group was in charge of dispensing justice in Texas -- the Texas Rangers. Many of the Texas Rangers were members of the Klan. Edward was the new master. Edward gained their loyalty by stroking their egos. Edward would use his money and influence to try and make them famous. Edward eventually inherited the Texas Ku Klux Klan.

Edward Mandell House helped to make four men governor of Texas: James S. Hogg (1892), Charles A. Culberson (1894), Joseph D. Sayers (1898), and S. W.T. Lanham (1902). After the election House acted as unofficial advisor to each governor. Hogg gave House the title "Colonel" by promoting House to his staff.

Edward wanted to control more than Texas, Edward wanted to control the country. Edward would do so by becoming a king maker instead of a king. Edward knew that if he could control two or three men in the Senate, two or three men in the House; and the President, he could control the country.

Edward would influence the candidate from behind the scenes. The people would perceive one man was representing them, when in reality; an entirely different man was in control. House didn't need to influence millions of people; he need only influence a handful of men. Edward would help establish a secret society in America that would operate in the same fashion -- the Council on Foreign Relations. Edward Mandell House was instrumental in getting Woodrow Wilson elected as President. Edward had the support of William Jennings Bryan and the financial backing of the House of Rockefeller's National City Bank. Edward became Wilson's closest unofficial advisor.

Edward Mandell House and some of his schoolmates were also members of Cecil Rhodes Round Table group. The Round Table Group, the back bone of the Secret Society, had four pet projects, a graduated income tax, a central bank, creation of a Central Intelligence Agency, and the League of Nations.

Between 1901 and 1913 the House of Morgan and the House of Rockefeller formed close alliances with the Dukes and the Mellons. This group consolidated their power and came to dominate other Wall Street powers including: Carnegie, Whitney, Vanderbilt, Brown-Harriman, and Dillon-Reed. The Round Table Group wanted to control the people by having the government tax people and deposit the peoples money in a central bank. The Group would take control of the bank and therefore have control of the money. The Group would take control of the State Department and formulate government policy, which would determine how the money was spent. The Group would control the CIA which would gather information about people, and script and produce psycho-political operations focused at the people to influence them to act in accord with Round Table Group State Department policy decisions. The Group would work to consolidate all the nations of the world into a single nation, with a single central bank under their control, and a single International Security System.

Some of the first legislation of the Wilson Administration was the institution of the graduated income tax (1913) and the creation of a central bank called the Federal Reserve. An inheritance tax was also instituted. These tax laws were used to rationalize the need for legislation that allowed the establishment of tax-exempt foundations. The tax-exempt foundations became the link between the Group member's private corporations and the University system. The Group would control the Universities by controlling the sources of their funding. The funding was money sheltered from taxes being channeled in ways which would help achieve Round Table Group aims.

1914

USA Open for Business

Congress ratifies the 16th Amendment creating the Internal Revenue Service. The amendment was proposed in Congress by Senator Nelson Aldrich.

As presented the income tax would only be one percent of income under $20,000, with the assurance that it would never increase.

Before the new central bank could begin operations,the Reserve Bank Organizing Committee, comprised of Treasury Secretary William McAdoo, Secretary of Agriculture David Houston, and Comptroller of the Currency John Skelton Williams, had the arduous task of building a working institution around the bare bones of the new law. But by Nov. 16,1914, the 12 cities chosen as sites for regional Reserve Banks were open for business, just as hostilities in Europe erupted into World War I.

1914-1919: Fed Policy during the War

When World War I broke out in mid-1914, U.S. banks continued to operate normally, thanks to emergency currency issued under the Aldrich-Vreeland Act of 1908.

Europe - World war breaks out in Europe. President Woodrow Wilson declares American neutrality.

Panama - The Panama Canal opens.

1915

USA

The British liner, "Lusitania" with 128 American passengers onboard and laden with munitions, cruised right through the middle of the wartime shipping lanes and was promptly sunk by a German submarine, thus bringing the U.S. directly into the European conflagration.

February 13, 1915 OPENS ACCEPTANCE BUSINESS TO BANKS; Federal Reserve Board Issues Regulations Governing Discount and Purchase. RAPID DEVELOPMENT LIKELY But Banks Are Cautioned to Move Slowly -- Extension Promised as Circumstances Warrant. Special to The New York Times.

But the greater impact in the United States came from the Reserve Banks' ability to discount banker's acceptances.

Through this mechanism,the United States aided the flow of trade goods to Europe, indirectly helping to finance the war until 1917, when the United States officially declared war on Germany and financing our own war effort became paramount.

"Wars are not fought to restrain communism or terrorism but to generate multibillion-dollar armaments contracts." ~ Antony C. Sutton

The net worth of the NWO international bankers is estimated to be $500 Trillion, more than half of the wealth of the entire world. They are the real rulers or the world. They have created every war in the last 100 years. American International Group

1917

USA February 12, The New York Times reported that:

"The five members of the Federal Reserve Board were impeached on the floor of the House by Rep. Charles A. Lindbergh, Republican member of the House Banking and Currency Committee. According to Mr. Lindbergh, 'the conspiracy began in' 1906 when the late J.P. Morgan, Paul M. Warburg, a present member of the Federal Reserve Board, the National City Bank and other banking firms 'conspired' to obtain currency legislation in the interest of big business and the appointment of a special board to administer such a law, in order to create industrial slaves of the masses, the aforesaid conspirators did conspire and are now conspiring to have the Federal Reserve Board administered so as to enable the conspirators to coordinate all kinds of big business and to keep themselves in control of big business in order to amalgamate all the trusts into one great trust in restraint and control of trade and commerce."

USSR The Soviets Get a Five-Year Plan

Professor Nickolai Kondratieff ( pronounced "Kon-DRA-tee-eff") helps develop the first Soviet Five-Year Plan . He analyzed factors that would stimulate Soviet economic growth.

World - The "Great War" (WWI) engulfs the world.

1918

USSR - Civil war broke out in Russia as the counter revolutionary White army attacked the communists.

1919

USA

Andrew Carnegie dies but not before giving away $350 million, over 90% of his wealth.

"The kept dollar is a stinking fish," — Andrew Carnegie

Germany - The Treaty of Versailles imposed war reparations on Germany.

Wales - Glyn Davies (full name Glyndwr Davies) is born in Abertillery in Monmouthshire, South Wales.

1920

USA

1920s: The Beginning of Open Market Operations and Technological Unemployment - US National Debt $25,952,456,406.

Following World War I, Benjamin Strong, head of the New York Fed from 1914 to his death in 1928, recognized that gold no longer served as the central factor in controlling credit. Strong's aggressive action to stem a recession in 1923 through a large purchase of government securities gave strong evidence of the power of open market operations to influence the availability of credit in the banking system. During the 1920s the Fed began using open market operations as a monetary policy tool. During his tenure, Strong also elevated the stature of the Fed by promoting relations with other central banks, especially the Bank of England.

On January 16 Prohibition took effect. It was the larggest boost for organized crime until the war on drugs.

The US Government cuts back on spending to balance the budget, which was spending three times more than tax revenues due to WWI.

The age of "Technological Unemployment" begins with as many as 200,000 workers a year replaced by automatic or semi-automatic machinery.

1921

USA

The Council on Foreign Relations (CFR) is founded by Edward Mandell House, who had been the chief advisor of President Woodrow Wilson.

1922

USA

The Supreme Court strikes down federal child labor legislation.

1923

USA

The business of America is business." — Calvin Coolidge

The Federal Reserve, under the direction of Benjamin Strong, head of the New York Fed, shifted toward a monetary policy of open market operations making a large purchase of government bonds.

The Teapot Dome scandal lands Secretary of Interior Albert Fall in jail.

President Warren Harding dies in office and Calvin Coolidge becomes president.

Canada - Clifford Hugh Douglas presents his ideas on "Social Credit" to the Canadian government before the Committee of the House of Commons on Banking and Industry.

1929

USA

1929-1933: The Market Crash and the Great Depression

During the 1920s Virginia Rep. Carter Glass warned that stock market speculation would lead to dire consequences. In October 1929 his predictions were realized when the stock market crashed, and the nation fell into the worst depression in its history. From 1930 to 1933 nearly 10,000 banks failed, and by March 6, 1933, newly inaugurated President Franklin Delano Roosevelt declared a bank holiday that lasted four days, while government officials grappled with ways to remedy the nation's economic woes. Many people blamed the Fed for failing to stem speculative lending that led to the crash, and some also argued that inadequate understanding of monetary economics kept the Fed from pursuing policies that could have lessened the depth of the Depression.

Herbert Hoover is inaugurated. More than half of all Americans are living below a minimum subsistence level. Annual per-capita income is $750; for people on farms, it is only $273.

The wave of about 1,200 mergers that had occurred during the decade had consolidated more than 6,000 companies.

In 1929 only 200 corporations will control over half of US industry.

Recession begins in August, two months before the stock market crash. During this two month period, production will decline at an annual rate of 20 percent, wholesale prices at 7.5 percent, and personal income at 5 percent.

The richest 1 percent own 40 percent of the nation's wealth. The bottom 93 percent have experienced a 4 percent drop in real disposable per-capita income during the period of 1923 to 1929.

The fist of many small crashes and recoveries in the stock market began on Monday, March 25. The FED started daily closed-door meetings.

On October 24, the large brokerages all simultaneously called-in their 24 hour "call-loans." The "Great Depression" begins October 24, 1929 and lasted until the late 1930s. The largest drop will occur on October 29, "Black Tuesday". Stock market losses for the month of October will total $16 billion.

The stock market crash and banking collapse in the United States sparks a global downturn, including a second downturn in the U.S., the Recession of 1937. During this time the Fed reduced the money supply by 33%.

"It was not accidental. It was a carefully contrived occurrence... The international bankers sought to bring about a condition of despair here so that they might emerge as rulers of us all." - Rep. Louis T. McFadden (D-PA)

"I think it can hardly be disputed that the statesmen and financiers of Europe are ready to take almost any means to re-acquire rapidly the gold stock which Europe lost to America as the result of World War I." - Rep. Louis T. McFadden (D-PA)

"The Federal Reserve definitely caused the Great depression by contracting the amount of currency in circulation by one-third from 1929 to 1933."- Milton Friedman, Nobel Prize winning economist

1930